How to Read a Medical Bill (Step-by-Step Guide)

Learn how to read a medical bill step by step. Understand your Explanation of Benefits (EOB), review charges, identify common billing issues, and make informed decisions before paying.

Introduction

You open your mailbox and pull out an envelope from the hospital.

You open it, look at the amount due, and immediately feel a knot in your stomach.

The bill is filled with unfamiliar medical terms, billing codes, insurance adjustments, and numbers that don't seem to make any sense. Maybe you expected your insurance to pay more. Maybe you don't understand why you're receiving another bill after you already paid one. Or maybe you're simply wondering whether the amount is even correct.

If that sounds familiar, you're not alone.

Every year, millions of Americans receive medical bills they don't fully understand. Many people assume the bill must be correct and pay it without asking questions. Others put it in a drawer because they don't know where to begin.

Neither approach is ideal.

The good news is that you don't need to work in healthcare or insurance to understand the basics of a medical bill. You simply need to know what you're looking for and which questions to ask.

That's exactly what this guide will teach you.

By the time you finish reading, you'll understand:

What information every medical bill should include

How to compare your bill with your insurance paperwork

Common billing mistakes to watch for

What different charges actually mean

What to do if something doesn't look right

When it may make sense to ask for help

The goal isn't to turn you into a medical billing expert.

The goal is to help you make informed decisions before you pay.

Sometimes you'll discover that your bill is completely accurate.

Other times, you'll find something that deserves a closer look.

Either way, spending a few minutes reviewing your bill can give you confidence that you're paying the right amount—and that peace of mind is worth the effort.

Let's start with the first thing you should check.

Why This Matters

Many people believe that medical bills are automatically correct.

Unfortunately, that's not always the case.

Healthcare billing is a complicated process involving hospitals, doctors, laboratories, insurance companies, and billing software. Every step in that process depends on information being entered accurately. Most of the time it is—but like any system managed by people, mistakes can happen.

That doesn't mean you should assume every medical bill contains an error.

It simply means you shouldn't assume every bill is correct without taking a few minutes to review it.

Think about it this way.

If your credit card statement included a charge you didn't recognize, you'd probably investigate before paying it.

The same idea applies to a medical bill.

Reviewing your bill isn't about trying to avoid paying what you legitimately owe. It's about making sure you understand the charges and confirming they're accurate.

A careful review can help you:

Better understand your insurance coverage

Identify questions to ask your provider

Catch possible billing issues

Learn about payment options that may be available

Feel more confident before paying

Even if you never find a single mistake, you'll leave with a much better understanding of how medical billing works.

And that's knowledge you can use every time you receive healthcare in the future.

What I'd Do First

If someone handed me a medical bill today, I wouldn't immediately look at the total balance.

I'd ask myself three simple questions:

Is this actually my bill?

Do I understand what this bill is for?

Has my insurance already processed it?

Only after answering those questions would I begin reviewing the individual charges.

That simple habit can save a surprising amount of confusion later.

Before We Begin

Throughout this guide, we'll occasionally refer to a fictional patient named Sarah.

Sarah recently visited the emergency room with severe abdominal pain. Over the next few weeks, she received several different medical bills from different providers.

We'll use Sarah's experience to show you exactly how to review a medical bill step by step.

Step 1: Start With the Basics

Before you worry about the dollar amount, take a minute to make sure you're looking at the right bill.

It sounds obvious, but this simple step can prevent a lot of confusion.

Medical bills often arrive weeks—or even months—after you receive care. If you've had multiple appointments, visited more than one provider, or received treatment over several days, it's easy to lose track of which bill belongs to which visit.

Start by checking these items.

Patient Name

Confirm that the bill is actually for you (or the family member you're responsible for).

Make sure:

Your name is spelled correctly.

The patient's name matches the person who received treatment.

There aren't two people with similar names in your household that could cause confusion.

If the patient information is wrong, don't ignore it.

Call the billing department and ask them to verify the account before making a payment.

Date of Service

The date of service tells you when you received medical care.

Ask yourself:

Does this date look familiar?

Was I actually treated on this day?

Is this the visit I expected to be billed for?

Many people receive multiple bills after a single hospital visit.

For example, one emergency room visit could result in separate bills from:

The hospital

The emergency physician

The radiologist

The laboratory

The ambulance company

Seeing several bills doesn't necessarily mean you've been billed twice.

It often means different providers are billing separately for the care they provided.

Provider Name

Who sent the bill?

This matters more than most people realize.

A bill from Milwaukee General Hospital is different from one sent by the physician group that staffed the emergency department.

Even if they relate to the same visit, they're usually handled by different billing departments.

If you're unsure who sent the bill, look for:

Provider name

Billing address

Phone number

Account number

Keep that information handy in case you need to call.

Account Number

Every bill has an account number or statement number.

Think of it as the bill's fingerprint.

If you call the billing office, this is usually the first thing they'll ask for.

A good habit is to write the account number at the top of any notes you take about the bill.

Balance Due

Now you can look at the balance.

Notice I said now.

Most people look at the total amount first.

I actually recommend the opposite.

If the first thing you see is:

Amount Due: $8,427.19

it's easy to become anxious and skip over the details.

Instead, make sure the bill belongs to you, understand what visit it's for, and identify who sent it.

Only then should you start reviewing the charges.

Sarah's Story

Let's go back to Sarah.

A week after her emergency room visit, she receives a bill for $2,846.13.

At first, she thinks:

"There's no way this can be right."

Instead of panicking, she slows down.

She checks:

✔ The patient's name

✔ The date she visited the emergency room

✔ The hospital name

✔ The account number

Everything matches.

So she knows she's looking at the correct bill.

Now she can move on to understanding what the bill actually says.

What I'd Do

If this were my own bill, I'd grab a pen or highlighter.

I'd circle:

Patient name

Date of service

Provider

Account number

Balance due

That gives me the key information I'll need if I end up calling the billing office.

I'd also create a folder—physical or digital—for everything related to this visit.

Keeping your bills, EOBs, and notes together will make the rest of the process much easier.

Common Mistake

One of the biggest mistakes people make is assuming that every bill they receive is a duplicate.

Imagine you go to the emergency room and later receive four separate bills.

Your first thought might be:

"They're charging me four times!"

In reality, you may have received bills from:

The hospital

The emergency physician

The radiologist who interpreted your CT scan

The laboratory that processed your blood work

Those are separate providers performing different services.

The important question isn't "Why did I receive four bills?"

It's:

"Do I understand what each bill is for?"

Once you can answer that question, you're ready for the next step.

Key Takeaway

Before you review a single charge, make sure you're looking at the correct bill.

Five minutes spent verifying the basics can prevent hours of confusion later.

Step 2: Compare Your Medical Bill to Your Explanation of Benefits (EOB)

If you only remember one thing from this guide, let it be this:

A medical bill and an Explanation of Benefits (EOB) are not the same thing.

This is one of the biggest sources of confusion for patients.

Many people receive an EOB from their insurance company, assume it's a bill, panic when they see a large number, and either throw it away or pay the wrong amount.

Let's clear up that confusion.

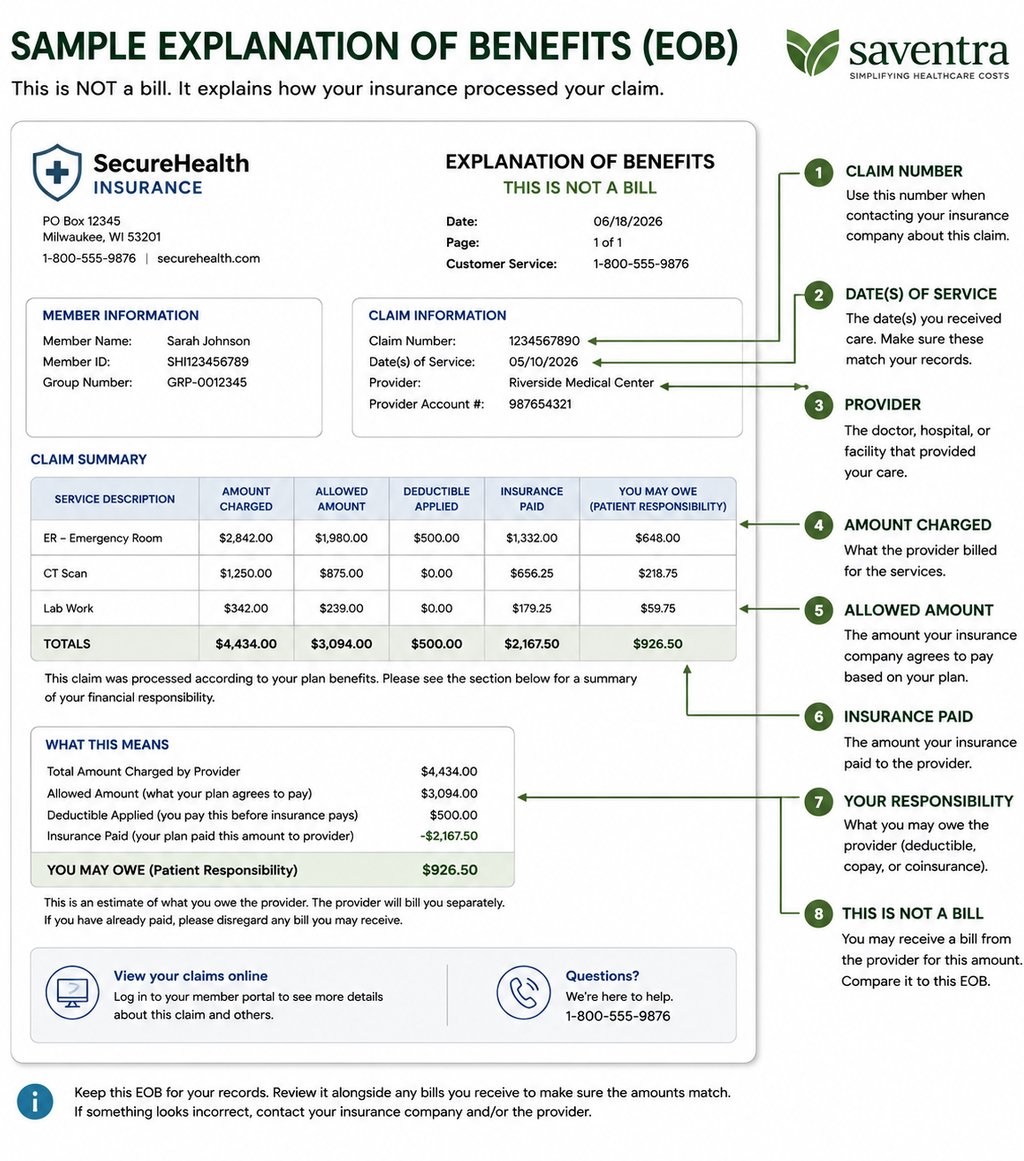

Example: What an Explanation of Benefits (EOB) Looks Like

This fictional Explanation of Benefits (EOB) highlights the information you'll typically find after your insurance company processes a claim. While the layout will vary between insurance companies, most EOBs contain similar information.

Important: An Explanation of Benefits is not a bill. It explains how your insurance company processed your claim and what you may owe. If you owe money, you'll typically receive a separate bill from your healthcare provider.

Medical Bill vs. Explanation of Benefits (EOB)

Many people confuse a medical bill with an Explanation of Benefits (EOB). While both relate to the same healthcare visit, they serve very different purposes. This quick comparison can help you tell them apart at a glance.

What Is an Explanation of Benefits (EOB)?

An Explanation of Benefits, often called an EOB, is a document sent by your health insurance company after they process a medical claim.

Despite the name, it isn't a bill.

It doesn't ask you to make a payment.

Instead, it explains how your insurance company handled the claim submitted by your healthcare provider.

Think of it as a receipt from your insurance company.

It answers questions like:

How much did the provider charge?

How much did the insurance company allow?

How much did insurance pay?

What portion may be your responsibility?

The provider's bill tells you what they're asking you to pay.

The EOB tells you why.

Why You Should Never Ignore Your EOB

Many people throw their EOB away because they think it's just more insurance paperwork.

That's a mistake.

Your EOB is one of the best tools you have for understanding your medical bill.

If something doesn't match, you have a reason to ask questions before paying.

Sarah's Story Continues

A few days after Sarah receives her hospital bill, she receives another envelope.

This one is from her health insurance company.

Across the top it says:

Explanation of Benefits

At first she worries.

"Great...another bill."

But after reading it more carefully, she realizes it isn't asking for payment.

Instead, it explains what happened after the hospital submitted its claim.

The hospital charged $2,846.13.

Sarah's insurance company determined that, under its contract with the hospital, the allowed amount was $1,975.00.

The insurance company paid $1,580.00.

The remaining amount—Sarah's deductible and coinsurance—was listed as her responsibility.

Now Sarah has something important she didn't have before.

She understands how the insurance company reached its decision.

Four Numbers You Should Compare

When reviewing your medical bill and EOB together, focus on these four numbers.

1. Provider Charges

This is the amount your healthcare provider billed before insurance adjustments.

Think of it as the starting point.

It isn't necessarily what you'll owe.

2. Allowed Amount

Insurance companies negotiate prices with many healthcare providers.

The allowed amount is the price your insurance recognizes under that agreement.

Often, it's lower than the provider's original charge.

Many patients never realize this adjustment even happened.

3. Insurance Payment

Next, look for how much your insurance company actually paid.

Sometimes it's nearly the entire bill.

Other times, the payment is smaller because of your deductible, coinsurance, or plan rules.

4. Your Responsibility

Finally, compare the amount your insurance company says you may owe with the amount shown on your provider's bill.

These numbers should generally make sense together.

If they don't, that's a good reason to ask questions.

What If They Don't Match?

Don't panic.

A difference doesn't automatically mean there's an error.

There are several possible explanations.

For example:

The provider billed before insurance finished processing the claim.

Insurance recently reprocessed the claim.

Another claim is still pending.

The provider hasn't updated its records yet.

Sometimes it's simply a timing issue.

Other times, it deserves a closer look.

The important thing is not to assume either document is wrong—or right—without asking.

What I'd Do

If I were reviewing my own bill, I'd put the medical bill and the EOB side by side.

Then I'd compare them line by line.

I'd ask myself:

Do the dates match?

Is this the same provider?

Has insurance already processed the claim?

Does the amount my insurance says I owe generally match what the provider is asking me to pay?

If the answer to any of those questions is "I'm not sure," that's where I'd start asking questions.

Common Mistake

One of the most common mistakes people make is paying the provider's bill before insurance has finished processing the claim.

Sometimes the provider sends an early statement simply because their billing system generated it automatically.

A week later, insurance finishes processing the claim and the balance changes.

Paying too early can create unnecessary confusion.

If you receive a bill shortly after receiving care, it's reasonable to ask:

"Has my insurance finished processing this claim?"

That one question can save a lot of frustration.

Pro Tip

Keep every EOB you receive.

Even after you've paid your bill.

If questions come up months later, your EOB provides a valuable record of how your insurance company processed the claim.

Many insurers also make EOBs available through their online member portals, making them easy to download if you need them again.

Key Takeaway

Your medical bill tells you what the provider is asking you to pay.

Your Explanation of Benefits tells you how your insurance company processed the claim.

Understanding both documents—and comparing them together—is one of the most important steps in reviewing a medical bill.

Step 3: Request an Itemized Bill

If your medical bill simply says:

Amount Due: $2,483.72

...it isn't telling you very much.

Imagine receiving your grocery receipt and seeing only:

Total: $184.63

No list of groceries.

No prices.

No quantities.

You'd probably want to know what you actually bought.

Medical bills work the same way.

An itemized bill breaks your charges into individual services so you can understand exactly what you're being billed for.

If your bill isn't itemized, requesting one is often one of the smartest first steps you can take.

What Is an Itemized Bill?

An itemized bill lists each service separately.

Instead of showing one large balance, it typically includes information such as:

The date each service was provided

A description of the service

The quantity

The charge for each service

Sometimes a billing or procedure code

This makes it much easier to understand your bill and ask informed questions.

Why Itemized Bills Matter

An itemized bill helps answer questions like:

Why is this bill so expensive?

What exactly am I paying for?

Were these services actually provided?

Does anything appear more than once?

Are there charges I don't recognize?

Without an itemized bill, it's difficult to review your bill in any meaningful way.

Sarah's Story Continues

Sarah calls the hospital's billing department.

"I'd like an itemized bill for my emergency room visit."

A few days later, she receives a new statement.

Instead of one balance, she now sees:

Emergency room facility charge

Blood work

CT scan

IV fluids

Laboratory testing

Physician evaluation

Now she can actually understand where the total came from.

She still isn't ready to pay.

But now she knows what questions to ask.

What Should You Look For?

As you review an itemized bill, don't try to become a medical coding expert.

Instead, focus on things that don't seem to make sense.

Ask yourself:

Did I receive this service?

If you don't remember receiving something, don't assume you're wrong.

Write it down.

Ask the provider to explain it.

Sometimes the explanation is simple.

Other times, it's worth investigating further.

Does Anything Appear Twice?

Sometimes the same service appears more than once.

That doesn't automatically mean it's a mistake.

For example, certain medications or treatments may legitimately be provided multiple times during a hospital stay.

But duplicate-looking charges deserve a closer look.

Ask:

"Can you explain why this service appears twice?"

Are the Dates Correct?

Check whether the dates match the care you received.

If you visited the emergency room on June 12, but one service shows June 18, ask why.

Sometimes there's a simple explanation.

Sometimes it's an administrative error.

Do the Quantities Make Sense?

Suppose your bill lists:

IV Bag — Quantity: 6

But you remember receiving one IV during a short emergency room visit.

That doesn't necessarily mean the bill is wrong.

It does mean it's reasonable to ask how that quantity was determined.

Are There Charges You Don't Understand?

Medical bills often include unfamiliar descriptions.

That's okay.

You aren't expected to know what every term means.

If something isn't clear, ask the billing department to explain it in plain language.

A good billing representative should be able to tell you:

What the service was

Why it was billed

When it was provided

What I'd Do

If I were reviewing my own bill, I'd use three different colors.

Green

I understand this charge.

Yellow

I'm not sure what this means.

Red

I definitely have a question about this.

That way, when I call the billing office, I already know exactly what I want to discuss.

It also makes the conversation much more organized.

Common Mistake

Many people assume that because they don't recognize a charge, it must be fraudulent.

Usually that's not the case.

Healthcare providers often use technical descriptions that aren't familiar to patients.

Instead of assuming something is wrong, start by asking for an explanation.

A simple conversation may clear up the confusion.

Pro Tip

Don't try to review your bill all at once.

If it's several pages long, take a break.

Review one page at a time.

A careful review is much more valuable than a rushed one.

Questions I'd Ask the Billing Department

When you call, consider asking:

Can you explain this charge?

Why was this service provided?

Why does this service appear twice?

Can you tell me what this billing code represents?

Has my insurance processed every charge?

Is this the final balance?

Can you send me an updated statement if anything changes?

These are straightforward, respectful questions that often provide the information you need.

Key Takeaway

An itemized bill turns one confusing balance into a detailed list of services.

You don't need to understand every medical term.

You simply need enough information to ask good questions and make sure the bill makes sense before you pay.

Step 4: Understand Why You Owe Money

One of the most frustrating parts of receiving a medical bill is seeing that you owe hundreds—or even thousands—of dollars even though you have health insurance.

Many people think:

"Why am I paying this? Isn't this what insurance is for?"

It's a fair question.

The answer is that health insurance doesn't always pay 100% of every medical bill.

Depending on your plan, you may be responsible for part of the cost.

The good news is that once you understand the basic terms, medical bills become much easier to understand.

Let's walk through them one by one.

Deductible

Your deductible is the amount you generally have to pay for covered healthcare services before your insurance begins paying its share (although many plans cover certain preventive services before the deductible).

Think of it like this.

Imagine your insurance plan has a $2,000 deductible.

If this is your first medical expense of the year and your bill is $600, you may be responsible for most or all of that $600 because you haven't yet met your deductible.

Later in the year, after you've paid enough medical expenses to satisfy the deductible, your insurance may begin sharing more of the costs.

The important point is this:

Having health insurance doesn't necessarily mean your first medical bills will be small.

Sarah's Story

Sarah has a $1,500 deductible.

Before her emergency room visit, she had only spent $300 on medical care that year.

That means she still had $1,200 of her deductible remaining.

When she receives her hospital bill, she's surprised that insurance didn't pay more.

After looking at her EOB, she realizes much of what she owes is because she hadn't yet met her deductible.

Nothing was necessarily wrong with the bill.

She simply didn't understand how her insurance worked.

That's a very common situation.

Copay

A copay (or copayment) is a fixed amount you pay for certain healthcare services.

For example:

$25 to visit your primary care doctor

$40 to see a specialist

$100 for an emergency room visit

The amount depends on your insurance plan.

Unlike a deductible, a copay is usually a fixed dollar amount.

Coinsurance

Coinsurance is the percentage of a covered medical expense that you pay after meeting your deductible.

Suppose your insurance pays 80% of covered charges.

Your coinsurance is 20%.

Here's a simple example.

A covered medical service costs $1,000.

After your deductible has been satisfied:

Insurance pays:

$800

You pay:

$200

That's your coinsurance.

Out-of-Pocket Maximum

📊 How Your Medical Bill Gets From the Provider to You

Understanding how a medical claim moves through the healthcare system can make it much easier to understand why you owe a balance. While every insurance plan is different, most claims follow a process similar to the one shown below.

This is one of the most important numbers in your health insurance plan.

Your out-of-pocket maximum is generally the most you'll pay for covered, in-network services during a plan year, after which your plan typically pays 100% of covered costs for the remainder of that period (subject to your plan's rules).

Once you reach that limit, your insurance company generally pays all remaining covered expenses for the rest of the plan year.

Many people never reach it.

But if you have major surgery, a hospitalization, or another expensive medical event, it can become very important.

Insurance Adjustments

This is one of the most misunderstood parts of a medical bill.

Imagine a hospital charges:

$8,000

Your insurance company has negotiated a lower price.

Instead of paying based on $8,000, it recognizes an allowed amount of $5,500.

The difference between those two numbers is often written off because of the contract between the provider and the insurer.

Patients sometimes see that adjustment and think:

"Did I just save $2,500?"

Not exactly.

It's simply part of how many insurance contracts work.

The important thing is that your responsibility is generally based on the allowed amount—not the original billed amount—when the provider is in-network.

Why Two People Can Receive Different Bills

This surprises many people.

Two patients can receive exactly the same treatment...

at the same hospital...

on the same day...

and still owe completely different amounts.

Why?

Because every insurance plan is different.

Factors that affect your bill include:

Your deductible

Your copays

Your coinsurance

Whether you've met your deductible

Whether the provider is in-network

The specific benefits included in your health plan

That's why it's difficult to compare your medical bill with someone else's.

What I'd Do

Whenever I receive a medical bill, I ask myself:

Am I paying this because:

I haven't met my deductible?

This is my copay?

This is my coinsurance?

Insurance didn't cover the service?

Something else?

Once I know why I owe money, the rest of the bill becomes much easier to understand.

Common Mistake

One of the biggest mistakes people make is assuming that every balance means insurance made a mistake.

Often, the balance is exactly what their insurance plan requires them to pay.

The goal isn't to assume the bill is wrong.

The goal is to understand why the balance exists.

Once you know that, you can decide whether it makes sense to ask additional questions.

Pro Tip

If you don't understand one of these insurance terms, don't be embarrassed.

Call your insurance company and ask them to explain it in plain English.

A good customer service representative should be able to explain:

Why you owe the amount you owe

How your deductible affected the claim

Whether your coinsurance was applied correctly

Whether the claim has been fully processed

Key Takeaway

Understanding why you owe money is just as important as understanding how much you owe.

Many balances are the result of deductibles, copays, coinsurance, or insurance adjustments—not necessarily billing errors.

Knowing the difference helps you ask better questions and make more informed decisions.

Step 5: Look for Common Medical Billing Errors

By now you've:

Verified that the bill belongs to you.

Compared it with your Explanation of Benefits (EOB).

Requested an itemized bill.

Learned why you owe money.

Now it's time to review the bill carefully.

Let's be clear about something before we begin.

Most medical bills are not full of errors.

Healthcare providers process thousands of claims every month, and the vast majority are handled correctly.

The purpose of reviewing your bill isn't to assume someone made a mistake.

It's to make sure you understand what you're being asked to pay and to identify anything that deserves a second look.

Think of this as a quality check—not a search for someone to blame.

6 Things Worth Reviewing on Every Medical Bill

This checklist highlights six areas worth reviewing before paying a medical bill. Not every issue indicates a billing mistake, but each is worth understanding if something doesn't look right.

Error #1: Duplicate Charges

Duplicate charges are exactly what they sound like.

The same service appears more than once on the bill.

Sometimes this is perfectly appropriate.

For example, if you received:

Three IV bags

Two X-rays

Multiple doses of medication

...you should expect multiple charges.

Other times, however, something appears twice when it shouldn't.

Imagine your itemized bill shows:

Chest X-Ray

$450

...

Later on the same bill...

Chest X-Ray

$450

Same date.

Same description.

That doesn't automatically mean it's wrong.

But it's absolutely worth asking about.

A simple question like:

"Can you help me understand why this service appears twice?"

is often the best place to start.

Error #2: Incorrect Patient Information

Sometimes the mistake has nothing to do with money.

Instead, it's basic information.

Check:

Your name

Date of birth

Address

Insurance information

If the wrong insurance company was billed, your balance could be much higher than it should be.

Fortunately, these types of mistakes are often straightforward to correct.

Error #3: Services You Don't Remember Receiving

This is one of the most common reasons people become concerned.

You see a description you've never heard before.

Your first thought is:

"I never received that."

Slow down.

Medical terminology is different from everyday language.

A service might simply be described differently than you expected.

For example:

A patient may not remember receiving:

IV Push Medication

But they do remember the nurse giving them medicine through their IV.

The wording is different.

The service may still be accurate.

The goal isn't to prove the bill is wrong.

The goal is to understand it.

If you still don't recognize a charge after it has been explained, that's when further questions make sense.

Sarah's Story

As Sarah reviews her itemized bill, she notices a charge called:

Comprehensive Metabolic Panel

She has no idea what that means.

Her first reaction is:

"I don't remember having that test."

Instead of assuming it was added by mistake, she calls the billing office.

The representative explains that it was one of the blood tests ordered by the emergency physician.

Suddenly the charge makes sense.

Nothing was wrong.

She simply didn't recognize the medical terminology.

That happens every day.

Error #4: Insurance Wasn't Applied Correctly

Sometimes the provider sends a bill before insurance has finished processing the claim.

Other times:

Insurance information wasn't updated.

The wrong policy number was used.

A secondary insurance plan wasn't billed.

The claim is still pending.

Before paying a large balance, it's reasonable to ask:

"Has my insurance finished processing this claim?"

That one question can save unnecessary frustration.

Error #5: Math Doesn't Make Sense

Sometimes the numbers simply don't add up.

For example:

Insurance payment

Patient responsibility

Adjustments

...should generally make sense together.

You don't need to perform complicated calculations.

Just ask yourself:

"Does this seem reasonable?"

If something looks inconsistent, ask the billing office to explain how the balance was calculated.

A good representative should be able to walk through it step by step.

What I'd Do

Whenever I review a bill, I don't try to find mistakes.

I try to understand the story.

I ask myself:

What happened?

What services did I receive?

What did insurance pay?

Why do I owe this amount?

If I can answer those questions confidently...

I'm usually comfortable moving forward.

If I can't...

That's where I start asking questions.

Notice the difference.

I'm looking for understanding—not problems.

Ironically, that's often the fastest way to discover issues if they exist.

Questions I'd Ask

Here are some questions that are polite, practical, and productive.

Instead of saying:

"This bill is wrong."

Try asking:

"Could you help me understand this charge?"

Instead of saying:

"You're charging me twice."

Try:

"Can you explain why this appears more than once?"

Instead of:

"Insurance didn't pay."

Ask:

"Has my insurance finished processing this claim?"

These questions invite a conversation instead of creating an argument.

Most billing representatives genuinely want to help, and a respectful approach often leads to a more productive discussion.

Pro Tip

Take notes during every phone call.

Write down:

The date

The time

The person's name

Their department

What they told you

Any promised follow-up

If you need to call again later, you'll be glad you did.

Key Takeaway

Reviewing your medical bill isn't about trying to catch someone making a mistake.

It's about understanding your bill well enough to recognize when something deserves clarification.

Most questions have simple answers.

Some reveal issues that can be corrected.

The only way to know the difference is to ask.

Step 6: What to Do If Something Doesn't Look Right

Let's say you've reviewed your bill.

You've compared it with your Explanation of Benefits (EOB).

You've requested an itemized bill.

You've gone through every charge.

But something still doesn't make sense.

What should you do?

The answer is simple:

Start by asking questions.

Don't assume the bill is wrong.

Don't assume it's right either.

Approach the situation with curiosity.

Your goal isn't to prove someone made a mistake.

Your goal is to understand your bill well enough to decide what to do next.

📞 Questions to Ask the Billing Department

Before calling the billing department, consider writing down your questions. Having them ready can help you stay organized and make the conversation more productive.

Start With the Billing Department

Your first call should usually be to the provider's billing department.

Why?

Because they have access to your account and can often answer questions immediately.

Before you call, gather:

Your medical bill

Your Explanation of Benefits (EOB)

Your account number

A notebook or document for taking notes

Being prepared makes the conversation much easier.

How to Start the Conversation

Many people feel nervous about calling.

They worry they'll sound uninformed.

Don't.

Billing representatives answer questions like yours every day.

A simple opening works well.

For example:

"Hi, I'm reviewing my medical bill and had a few questions. Could you help me understand a couple of the charges?"

Notice what this doesn't say.

It doesn't accuse.

It doesn't argue.

It simply asks for help.

That approach often leads to a much more productive conversation.

Questions Worth Asking

As you review your bill, you might ask:

About the Bill

Could you explain this charge?

What service does this represent?

Why was this service necessary?

Can you send me an itemized statement?

About Insurance

Has my insurance fully processed this claim?

Was the correct insurance billed?

Was this provider in-network?

Has a secondary insurance policy been billed?

About the Balance

How was my balance calculated?

Is this my deductible?

Is this coinsurance?

Are there any adjustments still pending?

About Payment

Do you offer payment plans?

Is financial assistance available?

Are there self-pay discounts?

Is there a prompt-pay discount if I pay in full?

Sometimes simply asking these questions reveals options you didn't know existed.

Sarah's Story Continues

Sarah still has one concern.

Her EOB says her responsibility should be approximately $395.

Her hospital bill still shows $790.

Instead of paying immediately, she calls the billing department.

The representative reviews her account.

After a few minutes, they discover the insurance payment had been received—but hadn't yet been applied to her account.

An updated statement is issued the next day.

Sarah didn't find a dramatic billing error.

She simply asked a good question at the right time.

Stay Organized

If your bill requires multiple phone calls, organization becomes your best friend.

Create a simple log.

Every time you speak with someone, write down:

Date

Time

Person's name

Department

Phone number (if available)

What was discussed

Any promised follow-up

It doesn't have to be fancy.

Even a notebook works.

These notes can be incredibly helpful if you need to reference a previous conversation later.

What If You Still Don't Understand?

Sometimes you've asked questions...

You've spoken with the billing office...

You've reviewed your paperwork...

...and you're still confused.

That's okay.

Medical billing can be complicated.

At that point, it may be worth asking for additional help from someone who regularly reviews medical bills.

A fresh set of eyes can often explain things that aren't immediately obvious.

What I'd Do

If this were my bill, I would follow a simple rule.

I wouldn't pay until I could answer these three questions confidently:

Do I understand what I'm being charged for?

Do I understand why I owe this amount?

Have all of my questions been answered?

If the answer to any of those questions was "no," I'd keep asking questions until I understood.

Not because I assume something is wrong...

But because I want to make an informed decision.

Common Mistake

One of the biggest mistakes people make is waiting until a bill is overdue before asking questions.

It's much easier to address concerns early than after the account has progressed through multiple billing cycles.

If something doesn't make sense, don't wait.

Reach out while the bill is still fresh.

Pro Tip

If someone promises to call you back, ask:

"When should I expect to hear from you?"

If that date passes without a response, call again and reference your previous conversation.

Being politely persistent is often more effective than waiting indefinitely.

Key Takeaway

Most billing questions can be resolved with a respectful conversation.

You don't need to be an expert.

You simply need to be organized, ask thoughtful questions, and understand the answers before deciding how to proceed.

Bringing It All Together

Let's look at everything we've learned so far.

If you receive a medical bill tomorrow, here's the process I would follow:

Step 1

Confirm the bill belongs to you.

Step 2

Compare it with your Explanation of Benefits.

Step 3

Request an itemized bill if you need more detail.

Step 4

Understand why you owe the balance.

Step 5

Review the bill carefully and ask questions about anything you don't understand.

Step 6

Speak with the billing department if something doesn't make sense.

Notice what isn't on this list.

Nowhere did we say:

"Assume the bill is wrong."

And nowhere did we say:

"Pay it immediately."

Instead, the goal is to make informed decisions.

That philosophy is at the heart of Saventra.

Step 7: What I'd Do If This Were My Medical Bill

We've covered a lot of information so far.

If someone handed me a medical bill today, here's exactly how I would approach it.

Not because I assume there's a problem.

But because I want to understand my bill before making a payment.

Let's walk through it together.

From Confusion to Confidence

Sarah's experience brings together everything you've learned throughout this guide. This simple timeline shows how reviewing your paperwork, asking questions, and understanding your bill can lead to informed decisions and greater confidence.

Day 1: Open the Bill

The first thing I'd do is actually open it.

That might sound obvious, but many people put medical bills aside because they're stressful.

The longer you wait, the harder it becomes to remember details about your visit.

Instead, I'd open it the day it arrives.

I don't have to solve everything immediately.

I simply want to understand what I'm looking at.

Day 1: Review the Basics

Before I even look at the amount due, I'd verify:

Is my name correct?

Is the date of service correct?

Do I recognize the provider?

Does this account number match my paperwork?

If something doesn't match, that's my first phone call.

Day 1: Gather My Paperwork

Before making any decisions, I'd collect everything related to that visit.

That includes:

Medical bills

Explanation of Benefits (EOBs)

Insurance letters

Receipts

Notes from previous conversations

Having everything in one place makes the review much easier.

Day 2: Compare Everything

Now I'd sit down with:

My medical bill

My EOB

My itemized bill (if I have one)

I'd compare them slowly.

Not looking for mistakes.

Looking for understanding.

I'd ask:

Do these dates match?

Does the provider match?

Did insurance process this claim?

Do I understand why I owe this amount?

If I can answer those questions...

I'm making progress.

Day 2: Highlight Questions

As I review the paperwork, I'd use a highlighter.

Green

"I understand this."

Yellow

"I'm not sure."

Red

"I definitely need to ask about this."

That way, I'm prepared before making any phone calls.

Day 3: Call the Billing Department

If I still have questions, I'd call.

Not to argue.

Not to complain.

Simply to understand.

I'd probably begin with something like:

"Hi, I'm reviewing my medical bill and hoped you could help me understand a few of the charges."

Notice the tone.

Friendly.

Respectful.

Specific.

People generally respond well when they feel you're trying to solve a problem together.

During the Call

While speaking with the billing department, I'd write down:

The representative's name

The date

The time

What they explained

Any promises they made

When they expect to follow up

Those notes become valuable if I need to call again.

If Everything Looks Correct

Sometimes that's the outcome.

The bill is accurate.

Insurance processed it correctly.

The balance makes sense.

That's actually good news.

Now I can make a decision with confidence instead of uncertainty.

If Something Doesn't Look Right

If I still don't understand the bill after speaking with the provider...

I'd continue asking questions.

Maybe I'd call my insurance company.

Maybe I'd ask for another explanation.

Maybe I'd request additional documentation.

The important thing is that I wouldn't guess.

If the Bill Is Correct but I Can't Afford It

This is a situation many people face.

If the amount is simply more than I can comfortably pay, I'd ask:

Do you offer payment plans?

Is financial assistance available?

Is there a prompt-pay discount?

Is there a self-pay discount?

Are there any other programs that might help?

Many providers have options that patients never discover because they never ask.

Sarah's Story Ends

Let's finish Sarah's story.

After reviewing her bill...

Comparing it with her EOB...

Requesting an itemized statement...

And speaking with the billing department...

She finally understands her balance.

Most of the amount she owes is due to her deductible.

One duplicate laboratory charge was corrected.

The insurance payment was properly applied.

She now knows exactly why she owes what she owes.

Most importantly...

She pays her bill with confidence.

Not because someone told her to.

Because she understands it.

That's the goal of this guide.

The Mindset I Hope You Take Away

If there's one thing I hope you remember after reading this guide, it's this:

Don't let confusion make your decisions for you.

Confusion causes people to:

Ignore bills.

Panic.

Pay immediately without reviewing them.

Assume something is wrong.

Assume everything is right.

None of those approaches are ideal.

Instead...

Slow down.

Review the information.

Ask questions.

Understand your options.

Then make an informed decision.

That's a much better way to approach any medical bill.

A Final Word Before We Wrap Up

Understanding a medical bill doesn't require years of experience.

It requires patience.

Organization.

And the willingness to ask questions.

The more often you review your bills carefully, the easier the process becomes.

Eventually you'll recognize common terms.

You'll understand your insurance better.

And you'll feel much more confident whenever a medical bill arrives.

That's a skill that can benefit you for years to come.

Frequently Asked Questions

1. Should I pay my medical bill immediately?

Not necessarily. Before making a payment, take a few minutes to review your bill, compare it with your Explanation of Benefits (EOB), and make sure you understand the charges. If something doesn't make sense, ask questions before paying.

2. What is the difference between a medical bill and an Explanation of Benefits (EOB)?

A medical bill is a request for payment from your healthcare provider.

An Explanation of Benefits (EOB) is a document from your insurance company explaining how your claim was processed. An EOB is not a bill.

3. Why did I receive more than one bill for the same visit?

It's common for multiple providers to bill separately after a single visit.

For example, you may receive separate bills from:

The hospital

The emergency physician

The radiologist

The laboratory

The anesthesiologist

Receiving multiple bills doesn't necessarily mean you've been billed twice.

4. Should I request an itemized bill?

If you don't clearly understand the charges on your bill, requesting an itemized bill is often a good idea. It provides a detailed breakdown of the services you were billed for and can make your bill much easier to review.

5. What if I don't recognize a charge?

Don't assume it's an error.

Medical terminology is often different from the language patients use every day. Start by asking the billing department to explain the charge in plain English. If you still have concerns after the explanation, continue asking questions.

6. What if my medical bill doesn't match my EOB?

Sometimes this is simply a timing issue. The provider may have sent the bill before your insurance company finished processing the claim or before payments were applied.

If the numbers don't make sense, contact the provider's billing department and ask them to explain the difference.

7. Can medical bills contain errors?

Mistakes can happen, but it's important not to assume every bill is incorrect. The goal is to review your bill carefully, understand the charges, and ask questions whenever something doesn't seem right.

8. What if I can't afford my medical bill?

If paying your bill would create a financial hardship, contact the provider as soon as possible. Ask whether they offer:

Payment plans

Financial assistance programs

Self-pay discounts

Prompt-pay discounts

Many providers have options available, but they often require patients to ask.

9. How long should I keep my medical bills and EOBs?

It's generally a good idea to keep copies of your medical bills, EOBs, receipts, and notes from billing conversations until you're confident the account has been fully resolved. Some people choose to keep these records longer for tax, insurance, or personal recordkeeping purposes.

10. Can I ask questions after I've already paid my bill?

Yes. If you discover something you don't understand after making a payment, you can still contact the provider's billing department and ask for an explanation.

11. What should I do if my insurance denies a claim?

Start by reviewing your Explanation of Benefits (EOB) to understand why the claim was denied. Then contact your insurance company or healthcare provider if you need clarification. Depending on the circumstances, you may have options to correct information or appeal the decision.

12. What's the difference between a deductible, a copay, and coinsurance?

Deductible: The amount you generally pay before your insurance begins sharing costs for covered services.

Copay: A fixed amount you pay for certain healthcare services.

Coinsurance: A percentage of the cost that you pay after your deductible has been met.

These terms work together to determine how much you owe for medical care.

13. How can I prepare before calling the billing department?

Have these items ready:

Your medical bill

Your Explanation of Benefits (EOB)

Your account number

A list of your questions

Something to take notes with

Being organized makes the conversation much easier.

14. When should I consider getting additional help reviewing my medical bill?

If you've reviewed your bill, compared it with your EOB, spoken with the provider, and still don't understand the charges, it may be helpful to have someone else review the situation with you. A second set of eyes can often provide clarity and help you better understand your options.

15. What is the most important thing to remember?

Don't let confusion make your decisions for you.

Take your time.

Review your paperwork.

Ask questions.

Understand your options.

Then make an informed decision about your medical bill.

The Saventra Bill Review Checklist

Reviewing a medical bill can feel overwhelming, especially if you've never done it before. To make the process easier, we've created the Saventra Bill Review Checklist. Save it, print it, or keep it nearby whenever you're reviewing a medical bill.

Need Another Set of Eyes?

Understanding a medical bill isn't always easy. Even after reviewing your bill carefully, you may still have questions about your charges, your insurance, or what to do next.

That's why Saventra offers a free 10-minute assessment.

We'll take a few minutes to understand your situation, answer your initial questions, and let you know whether our medical bill review service may be able to help.

Whether you decide to work with us or not, our goal is the same: to help you better understand your healthcare costs so you can make informed decisions.

Schedule Your Free 10-Minute Assessment

References & Additional Resources

The information in this guide is based on educational resources from trusted organizations, including:

While every effort has been made to provide accurate and up-to-date educational information, medical billing and insurance policies can vary by provider, insurance plan, and state. This guide is intended for general educational purposes only and should not be considered legal, medical, tax, or insurance advice.

If you're unsure about your specific situation, contact your healthcare provider, your health insurance company, or another qualified professional for guidance.