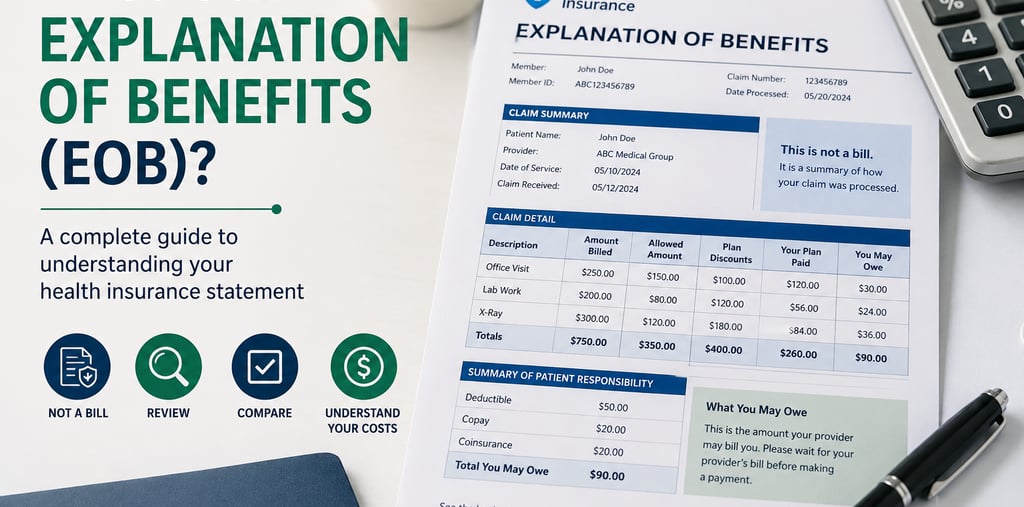

What Is an Explanation of Benefits (EOB)? Everything You Need to Know

Learn what an Explanation of Benefits (EOB) is, how to read it, what each section means, and how to compare it with your medical bill to catch costly mistakes.

INSURANCE & EOBS

My post content

What Is an Explanation of Benefits (EOB)? Everything You Need to Know

After a doctor's appointment, hospital visit, surgery, or other medical care, you may receive a document from your health insurance company called an Explanation of Benefits, often shortened to EOB.

If you've never seen one before, it can be confusing.

It isn't a bill, yet it lists dollar amounts. It explains what your insurance company paid, but it may also show that you could owe money. It contains unfamiliar insurance terms, medical billing codes, and several different numbers that don't always seem to match the medical bill you eventually receive.

If you've ever looked at an Explanation of Benefits and wondered, "What am I supposed to do with this?", you're not alone.

The good news is that understanding an EOB is easier than it first appears.

An Explanation of Benefits is one of the most valuable documents you'll receive after medical care because it helps you understand how your insurance company processed your claim. It can also help you identify questions, spot potential billing issues, and better understand what you may actually owe before paying a medical bill.

In this guide, you'll learn:

What an Explanation of Benefits (EOB) is

Why your insurance company sends one

Why an EOB is not a medical bill

How to read each section of an EOB

The five numbers you should always review

How to compare an EOB with your medical bill

Common mistakes and red flags to watch for

What to do if something doesn't look right

Whether you've received your first Explanation of Benefits or simply want to better understand your health insurance, this guide will walk you through the process step by step in plain English—no insurance expertise required.

Table of Contents

What Is an Explanation of Benefits (EOB)?

Is an Explanation of Benefits a Bill?

Why Do Insurance Companies Send EOBs?

When Will You Receive an EOB?

Every Section of an Explanation of Benefits Explained

The 5 Numbers You Should Always Check on Every Explanation of Benefits

How to Compare Your EOB to Your Medical Bill

Common Explanation of Benefits Mistakes and Red Flags

What Should You Do If Something Looks Wrong?

Frequently Asked Questions

Final Thoughts

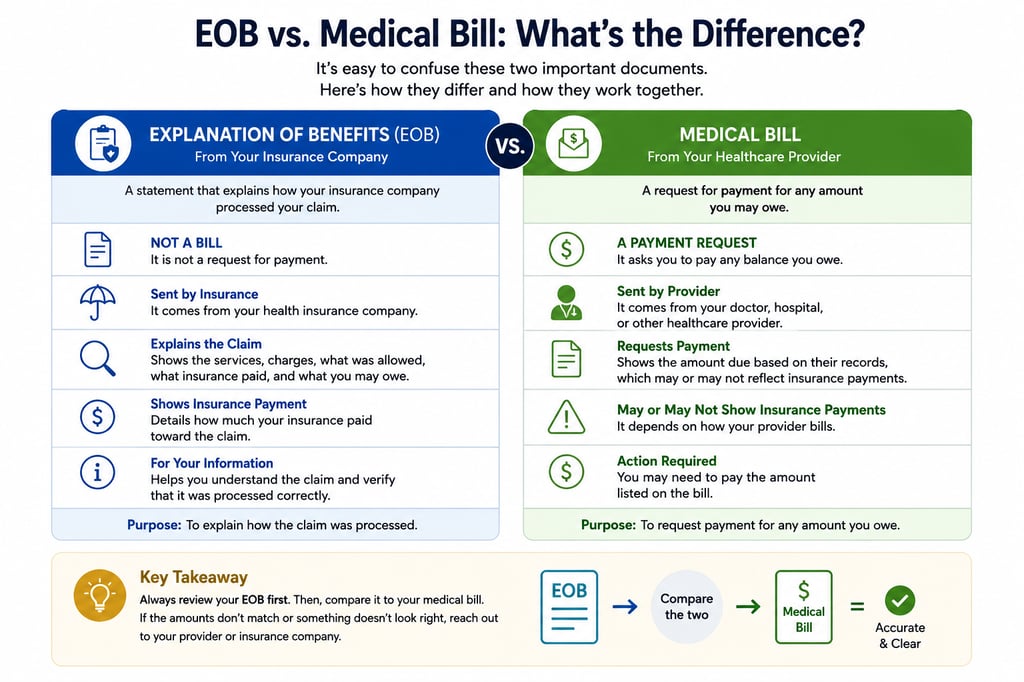

Is an Explanation of Benefits (EOB) a Bill?

One of the most common sources of confusion is that an Explanation of Benefits (EOB) is not a bill.

Although an EOB may contain dollar amounts and show that you could be responsible for part of the cost of your medical care, it is not a request for payment from your insurance company.

Instead, it is a summary explaining how your insurance company processed your claim.

Many people receive an EOB before they receive a bill from their healthcare provider. This often leads them to believe they need to pay the amount listed immediately. In most cases, that's not true.

Your healthcare provider will typically send a separate medical bill if you owe money after your insurance company finishes processing the claim.

Think of it this way:

The EOB explains what happened.

The medical bill requests payment.

The two documents work together, but they serve different purposes.

A Simple Example

Imagine you visit your primary care physician for an office visit.

After your appointment:

Your doctor submits a claim to your insurance company.

Your insurance company reviews the claim and determines what your health plan covers.

Your insurance company sends you an Explanation of Benefits explaining how the claim was processed.

If you owe any remaining balance, your doctor's office later sends you a medical bill requesting payment.

Because these documents often arrive days or even weeks apart, it's easy to mistake one for the other.

Why the Confusion Happens

Many Explanation of Benefits statements include language such as:

"You May Owe: $150.00"

Seeing that number naturally makes people think they're expected to pay their insurance company.

In reality, that amount is simply the insurance company's estimate of your financial responsibility based on how the claim was processed. It is not a payment request.

Your healthcare provider is the one that determines the final bill you'll receive after accounting for your insurance payment.

That's why it's important to wait until you've received both your Explanation of Benefits and your medical bill before making a payment.

When the Amounts Don't Match

Sometimes the amount listed on your Explanation of Benefits matches your medical bill exactly.

Other times, it doesn't.

There are several legitimate reasons why this can happen, including:

The provider submitted additional claims after the EOB was issued.

More than one provider billed separately for your care.

Your insurance company reprocessed the claim.

The provider corrected billing information after the original claim was submitted.

However, differences between your EOB and your medical bill can also signal a billing or insurance issue that deserves a closer look.

Before paying a medical bill, compare it with your Explanation of Benefits to make sure:

The patient information matches.

The dates of service are correct.

The provider names are accurate.

The services listed appear consistent.

The insurance payment matches what your insurer reported.

Your financial responsibility appears reasonable.

If something doesn't look right, don't assume the bill is automatically correct. Contact your healthcare provider's billing office or your insurance company and ask questions before making a payment.

Key Takeaway

An Explanation of Benefits is not a bill—it is an explanation.

Its purpose is to help you understand how your insurance company processed your claim. Your medical bill, on the other hand, is the document that requests payment from you.

Reviewing both documents together gives you the clearest picture of what happened, what your insurance covered, and what you may actually owe.

Why Do Insurance Companies Send Explanation of Benefits (EOBs)?

If an Explanation of Benefits isn't a bill, you might be wondering why your insurance company sends one at all.

The answer is simple: an EOB helps you understand how your health insurance claim was processed.

Every time a healthcare provider submits a claim to your insurance company, several important decisions are made behind the scenes. Your insurance company reviews the services that were billed, determines what your health plan covers, calculates any discounts that apply under your policy, and decides what portion of the costs may become your responsibility.

Rather than keeping those decisions hidden, your insurance company summarizes them in an Explanation of Benefits.

Think of your EOB as a detailed receipt—not for payment, but for how your insurance benefits were applied.

An EOB Promotes Transparency

Healthcare billing can be complicated.

A single doctor's visit may involve multiple providers, different billing codes, negotiated insurance rates, and several separate claims. Without an Explanation of Benefits, you would have very little insight into how your insurance company arrived at the amount it paid—or why you might owe anything at all.

Your EOB helps make that process more transparent by showing:

The services that were submitted for payment

The amount charged by your healthcare provider

The amount your insurance company allowed under your plan

What your insurance company paid

Any portion that may become your responsibility

This information gives you an opportunity to verify that everything appears accurate before paying a medical bill.

An EOB Helps You Catch Errors

No billing system is perfect.

Although many claims are processed correctly, mistakes can happen at several points during the healthcare billing process. An incorrect billing code, duplicate claim, missing insurance information, or processing error can all affect what your insurance pays and what you ultimately owe.

Your Explanation of Benefits serves as an early opportunity to spot potential problems.

For example, while reviewing your EOB, you might notice:

A service you don't remember receiving

The wrong date of service

An unfamiliar healthcare provider

Insurance that appears not to have been applied correctly

A claim that was denied unexpectedly

Identifying these issues early can make them easier to resolve before they become larger billing problems.

An EOB Helps Protect Against Fraud

Another important purpose of an Explanation of Benefits is helping detect healthcare fraud and identity theft.

Although uncommon, there are situations where claims are submitted for services that were never provided or where someone else's medical information becomes associated with your insurance account.

Reviewing each EOB allows you to confirm that:

You actually received the healthcare services listed.

The provider names are familiar.

The dates of service are accurate.

The procedures generally match the care you received.

If something looks unfamiliar, contact both your insurance company and the healthcare provider as soon as possible to ask for clarification.

An EOB Helps You Track Your Healthcare Costs

Over time, your Explanation of Benefits also becomes a valuable financial record.

Because each EOB summarizes a medical claim, keeping copies can help you:

Track your healthcare spending throughout the year.

Understand how much your insurance has paid.

Monitor your progress toward your deductible and out-of-pocket maximum.

Keep organized records if billing questions arise later.

Many insurance companies also make past EOBs available through their online member portals, making it easier to review previous claims whenever you need them.

Should You Read Every Explanation of Benefits?

Yes.

You don't necessarily need to study every line in detail, but it's a good habit to review each Explanation of Benefits shortly after receiving it.

Even a quick review can help you answer several important questions:

Does this claim belong to me?

Do I recognize the provider?

Do the dates look correct?

Does the care generally match what I received?

Does anything seem unusual?

Most EOBs can be reviewed in just a few minutes, and that small investment of time may help you identify billing or insurance issues before they become much more difficult to resolve.

Key Takeaway

An Explanation of Benefits isn't just paperwork—it's one of the most useful tools you have for understanding how your health insurance handled a medical claim.

By reviewing each EOB, you can better understand your healthcare costs, verify that your insurance benefits were applied correctly, identify potential billing errors, and catch possible fraud before it creates bigger problems.

When Will You Receive an Explanation of Benefits (EOB)?

Many people are surprised when an Explanation of Benefits arrives days—or even weeks—after they've received medical care. Others are confused when they receive a medical bill before their EOB or wonder why nothing has arrived at all.

The timing depends on how quickly your healthcare provider submits the claim and how long it takes your insurance company to process it.

Although every situation is different, most medical claims follow the same general process.

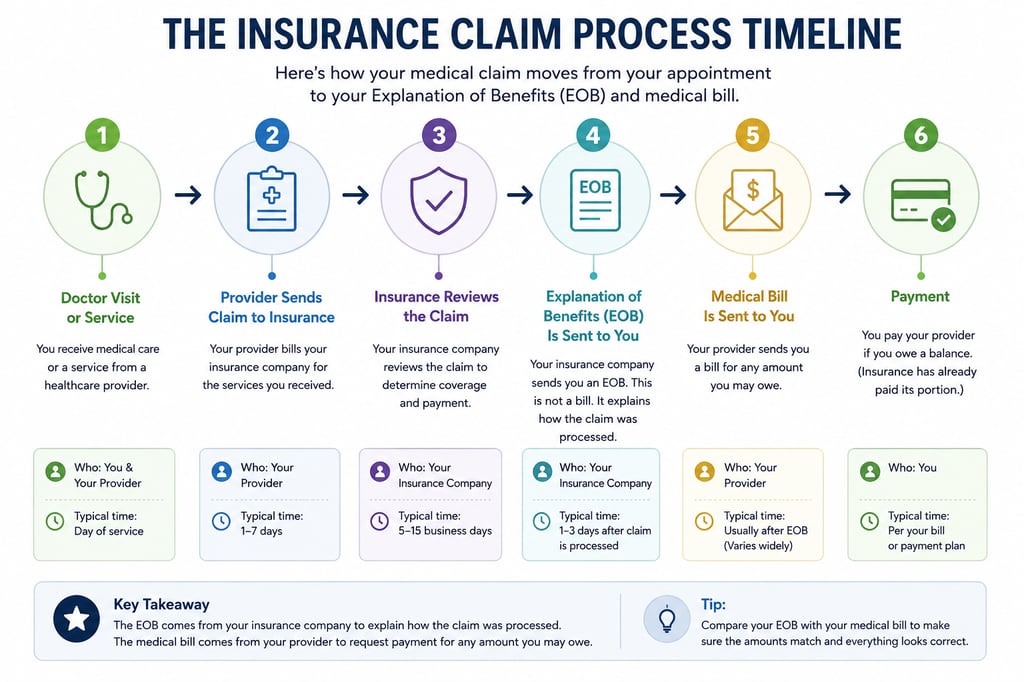

A Typical Insurance Claim Timeline

Understanding the sequence of events can make it much easier to know what documents to expect and when.

Step 1: You Receive Medical Care

Everything begins when you receive healthcare services.

This might include:

A visit to your primary care physician

An urgent care visit

Emergency room treatment

Laboratory testing

Medical imaging, such as an X-ray or MRI

Surgery

Physical therapy

A specialist appointment

At this point, you usually won't receive an Explanation of Benefits because your insurance company hasn't yet received a claim.

Step 2: Your Healthcare Provider Submits a Claim

After your visit, your healthcare provider prepares and submits a claim to your health insurance company.

The claim typically includes information such as:

Your personal information

Your insurance information

The date of service

The medical services provided

Billing codes used to describe those services

The amount charged by the provider

Depending on the provider, this may happen within a few days—or it may take several weeks.

Step 3: Your Insurance Company Reviews the Claim

Once your insurance company receives the claim, it reviews the information and determines how your health plan applies.

During this review, the insurer may determine:

Whether the services are covered under your plan

Whether any prior authorization requirements were met

Whether your deductible applies

Whether coinsurance or copays apply

The negotiated amount allowed under your insurance contract

The amount the insurance company will pay

If additional information is needed, the insurance company may request clarification from the provider before finalizing the claim.

Step 4: Your Insurance Company Sends Your Explanation of Benefits

After processing the claim, your insurance company generates your Explanation of Benefits.

The EOB summarizes how the claim was handled and explains:

What your provider billed

What your insurance allowed

What your insurance paid

What portion may become your responsibility

Many insurance companies now make EOBs available through their online member portals before a paper copy arrives in the mail.

Step 5: Your Healthcare Provider Sends Your Medical Bill

If you still owe money after your insurance processes the claim, your healthcare provider will typically send you a medical bill.

This often arrives several days or weeks after the Explanation of Benefits—but not always.

Sometimes the bill arrives first.

Sometimes both documents arrive around the same time.

Occasionally, you'll receive revised bills or updated EOBs if the claim is corrected or reprocessed.

Why Did My Medical Bill Arrive Before My EOB?

This is one of the most common questions patients ask.

There are several reasons why this can happen.

For example:

Your provider mailed the bill before your insurance company mailed the EOB.

Your insurance company is still processing part of the claim.

Multiple providers billed separately.

The provider generated an initial statement before receiving the insurance payment.

Receiving a medical bill before your Explanation of Benefits doesn't necessarily mean something is wrong.

However, unless your bill has an immediate due date or you've confirmed the balance with your insurance company, it's often reasonable to wait until you've reviewed your Explanation of Benefits so you can compare the two documents.

If you're unsure, contact your provider's billing office and let them know you're waiting for your insurance to finish processing the claim.

What If You Never Receive an Explanation of Benefits?

If several weeks have passed since your medical visit and you haven't received an Explanation of Benefits, consider taking a few simple steps:

Check your health insurance company's online member portal.

Confirm that your provider submitted the claim to your insurance company.

Verify that your insurance information was correct at the time of your visit.

Contact your insurance company to ask whether the claim has been received or is still being processed.

Sometimes the delay is simply administrative. In other cases, correcting missing or incorrect insurance information may allow the claim to move forward.

Key Takeaway

An Explanation of Benefits doesn't arrive immediately after your medical visit because it can't be created until your healthcare provider submits a claim and your insurance company finishes processing it.

Understanding this timeline can help you know what documents to expect, why they may arrive in a different order than expected, and why it's often helpful to compare your Explanation of Benefits with your medical bill before making a payment.

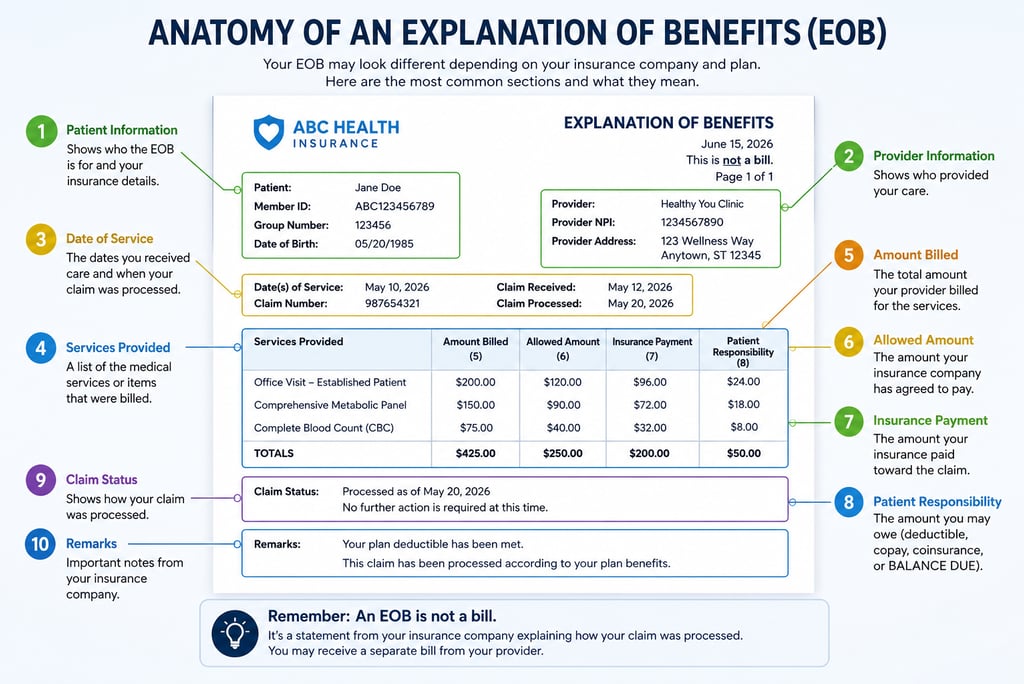

Every Section of an Explanation of Benefits (EOB) Explained

At first glance, an Explanation of Benefits can seem overwhelming. Most EOBs contain dozens of numbers, medical terms, billing codes, and insurance terminology that aren't immediately obvious.

The good news is that you don't need to understand every line on the page.

If you know what the major sections mean and how they work together, you'll be able to review your Explanation of Benefits with much more confidence.

While the layout varies from one insurance company to another, nearly every EOB contains the same core information.

Let's walk through each section.

Patient Information

Near the top of your Explanation of Benefits, you'll usually find information identifying who the claim belongs to.

This typically includes:

Patient name

Member name (if different)

Insurance ID number

Claim number

This may seem like a minor detail, but it's an important place to start.

Before reviewing any of the financial information, make sure the claim actually belongs to you or your covered family member.

If the wrong patient appears on the Explanation of Benefits, contact your insurance company immediately.

Provider Information

Your Explanation of Benefits also identifies the healthcare provider that submitted the claim.

Depending on the type of medical care you received, this might be:

Your primary care physician

A specialist

A hospital

An urgent care clinic

An imaging center

A laboratory

An ambulance company

One surprise for many patients is that a single medical visit can generate multiple Explanation of Benefits from different providers.

For example, after visiting an emergency room, you might later receive separate claims for:

The hospital

The emergency physician

The radiologist

The laboratory

The ambulance service

Each provider may bill independently.

That means multiple EOBs for the same date of service are often completely normal.

Date of Service

The Date of Service tells you when you actually received medical care.

Compare this carefully with your own records.

Ask yourself:

Do I remember receiving care on this date?

Does it match my appointment?

Was I hospitalized during this period?

If the date looks unfamiliar, it's worth asking questions before paying any related bill.

Description of Services

Most Explanation of Benefits statements include a brief description of the healthcare services that were billed.

Examples might include:

Office visit

Emergency room evaluation

Blood test

X-ray

MRI

Surgery

Physical therapy

Sometimes these descriptions are written in plain English.

Other times they may appear as medical billing codes with limited descriptions.

Don't worry if you don't recognize every term.

Instead, ask yourself:

Does this generally describe the care I received?

If something appears completely unfamiliar, contact your provider's billing office for clarification.

Amount Billed

This is the amount your healthcare provider originally charged for the services they provided.

Many patients assume this is the amount they will owe.

In reality, it rarely is.

The Amount Billed represents the provider's initial charge before insurance discounts or benefit calculations are applied.

For insured patients, this number is often much higher than the final amount used to calculate payment.

Allowed Amount

The Allowed Amount is one of the most important numbers on your Explanation of Benefits.

It represents the amount your insurance company recognizes as eligible for payment under its agreement with your healthcare provider.

If your provider is in-network, this amount is usually lower than the provider's original billed charge because insurance companies negotiate contracted rates with participating providers.

The difference between the Amount Billed and the Allowed Amount is often one of the largest reductions you'll see on an Explanation of Benefits.

Insurance Payment

This section shows how much your insurance company paid toward the claim.

Depending on your health plan, insurance may pay:

The full allowed amount

A portion of the allowed amount

Nothing at all

A payment of zero doesn't automatically mean something went wrong.

There are several possible reasons, including:

Your deductible hasn't been met.

The service isn't covered by your plan.

The claim was denied.

Additional information is needed before payment can be made.

The Explanation of Benefits usually includes additional notes explaining why.

Patient Responsibility

Near the bottom of most Explanation of Benefits statements, you'll find an estimate of what you may owe.

This amount often includes things like:

Copays

Deductibles

Coinsurance

Non-covered services

It's important to remember that this section is not a bill.

Instead, it reflects the insurance company's estimate of your financial responsibility based on how it processed the claim.

Always compare this amount with the medical bill you later receive from your healthcare provider.

Claim Status

Most Explanation of Benefits statements also indicate the current status of the claim.

Common examples include:

Paid

Processed

Pending

Denied

Adjusted

If your claim was denied, don't panic.

A denial doesn't always mean you'll be responsible for the full amount.

Sometimes claims are denied because:

Information was missing.

Additional documentation was required.

A coding issue needs correction.

The provider needs to resubmit the claim.

We'll discuss claim denials in more detail later in this guide.

Remark Codes and Notes

Near the bottom of many Explanation of Benefits statements, you'll often see remark codes or explanatory notes.

These provide additional context about how the claim was processed.

Examples might explain:

Why part of a claim wasn't covered.

Why additional documentation is needed.

Why the provider must adjust the bill.

Whether another insurance company should process the claim first.

Although these notes can seem technical, they're often the key to understanding why your insurance company made a particular decision.

If something isn't clear, don't hesitate to ask your insurance company what a remark code means.

Don't Focus on Every Number

One mistake many people make is trying to understand every single line of their Explanation of Benefits.

That's usually unnecessary.

Instead, focus on answering these questions:

✓ Is this my claim?

✓ Do I recognize the provider?

✓ Does the date of service look correct?

✓ Do the services generally match the care I received?

✓ Does the insurance payment make sense?

✓ Does my estimated responsibility seem reasonable?

If the answers to those questions are "yes," your claim was likely processed correctly.

If something seems unusual, it's worth investigating before paying a medical bill.

Key Takeaway

You don't need to become an insurance expert to review an Explanation of Benefits effectively.

By understanding the major sections—who received care, who provided it, what services were billed, what insurance paid, and what you may owe—you can quickly identify potential issues and feel much more confident when reviewing your healthcare costs.

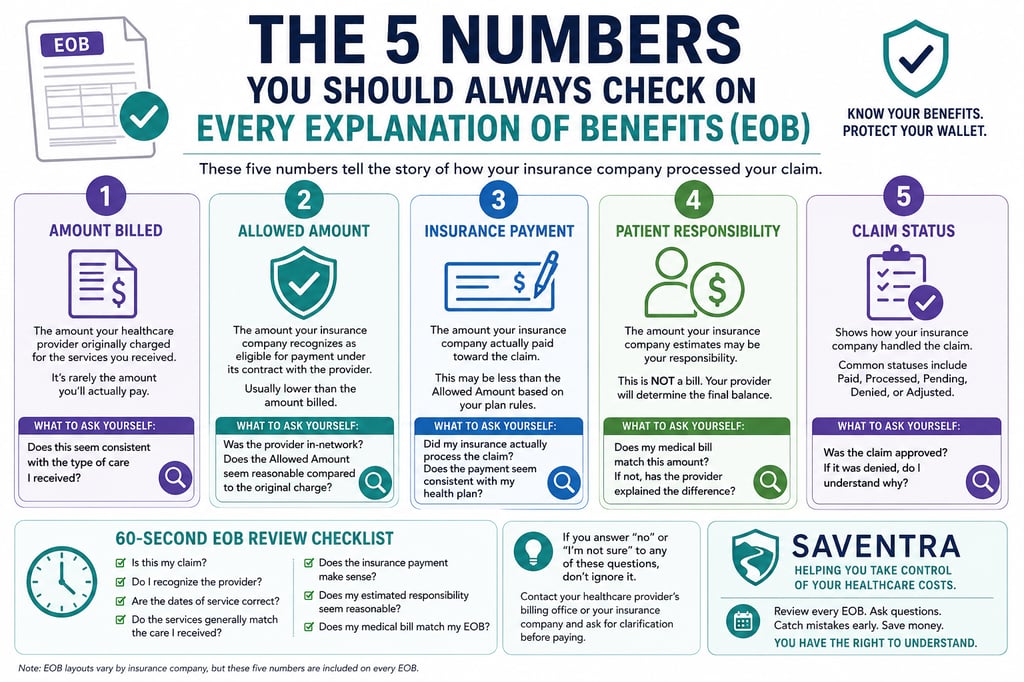

The 5 Numbers You Should Always Check on Every Explanation of Benefits (EOB)

If you only spend a few minutes reviewing your Explanation of Benefits, don't try to read every line.

Instead, focus on these five key numbers.

Together, they tell the story of how your insurance company processed your claim and whether anything deserves a closer look.

1. Amount Billed

The Amount Billed is the price your healthcare provider originally charged for the services you received.

For many people, this is the largest number on the page—and it's often the most alarming.

Fortunately, it's usually not the amount you'll actually pay.

Healthcare providers often bill significantly more than the negotiated rates they've agreed to accept from insurance companies.

What to ask yourself

Does this seem consistent with the type of care I received?

Was this claim submitted by the provider I expected?

Remember, the Amount Billed is simply the provider's starting point. The remaining numbers on your EOB determine what happens next.

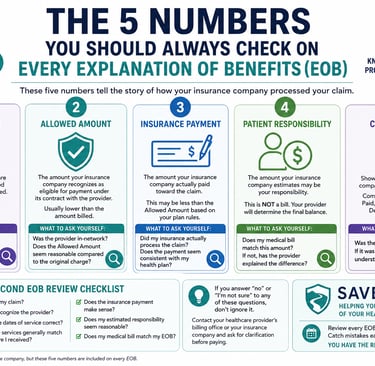

2. Allowed Amount

The Allowed Amount is one of the most important numbers on your Explanation of Benefits.

This is the amount your insurance company recognizes as eligible for payment under its contract with the provider.

If your provider is in-network, the Allowed Amount is often much lower than the Amount Billed because insurance companies negotiate discounted rates.

For example:

Provider billed:

$2,000

Insurance allowed:

$850

The provider generally agrees to accept the Allowed Amount as payment (subject to your deductible, copay, or coinsurance), rather than the full billed charge.

What to ask yourself

Was the provider in-network?

Does the Allowed Amount seem reasonable compared with the original charge?

3. Insurance Payment

Next, look at what your insurance company actually paid.

This number reflects the portion of the Allowed Amount that your insurance plan covered after applying your policy's rules.

Don't be surprised if the insurance payment is less than the Allowed Amount.

That doesn't necessarily mean something is wrong.

Several factors can affect the payment, including:

Your deductible

Copays

Coinsurance

Annual benefit limits

Services that aren't covered

What to ask yourself

Did my insurance actually process the claim?

Does the payment seem consistent with my health plan?

4. Patient Responsibility

This is the number most people look for first.

It represents the amount your insurance company estimates may become your responsibility.

Notice the word may.

An Explanation of Benefits is not a bill.

Your healthcare provider will determine the final balance after insurance processing is complete.

Before paying anything, compare this number with the medical bill you receive.

If the two amounts are significantly different, it's worth asking why.

What to ask yourself

Does my medical bill match this amount?

If not, has the provider explained the difference?

5. Claim Status

Finally, check the claim status.

This tells you how your insurance company handled the claim.

Common statuses include:

Paid

Processed

Pending

Denied

Adjusted

A denied claim doesn't always mean you'll owe the full amount.

Claims are denied for many reasons, including:

Missing documentation

Incorrect billing codes

Eligibility issues

Prior authorization requirements

Clerical mistakes

Many denials can be corrected and resubmitted.

What to ask yourself

Was the claim approved?

If it was denied, do I understand why?

A Simple 60-Second EOB Review Checklist

Whenever you receive an Explanation of Benefits, ask yourself these questions:

☐ Is this my claim?

☐ Do I recognize the provider?

☐ Are the dates of service correct?

☐ Do the services generally match the care I received?

☐ Does the insurance payment make sense?

☐ Does my estimated responsibility seem reasonable?

☐ Does my medical bill match my EOB?

If you answer "no" or "I'm not sure" to any of these questions, don't ignore it. Contact your healthcare provider's billing office or your insurance company and ask for clarification before paying.

Key Takeaway

You don't need to understand every line on your Explanation of Benefits.

By reviewing just five key numbers—the Amount Billed, Allowed Amount, Insurance Payment, Patient Responsibility, and Claim Status—you can quickly understand how your claim was processed and identify issues that may deserve a closer look.

How to Compare Your Explanation of Benefits (EOB) to Your Medical Bill

Receiving both an Explanation of Benefits and a medical bill can be confusing, especially when the numbers don't appear to match at first glance.

That's why one of the most valuable things you can do before paying a medical bill is compare it with your EOB.

Doing so helps confirm that your insurance processed the claim correctly, that your provider billed you appropriately, and that the amount you're being asked to pay makes sense.

The good news is that you don't need to be a medical billing expert to perform a basic review.

Start by comparing these seven items.

1. Patient Information

Begin with the basics.

Verify that both documents belong to the same person.

Check:

Patient name

Insurance member (if listed)

Date of birth, if applicable

While mistakes are uncommon, they can happen.

If the patient information doesn't match, contact your healthcare provider before making a payment.

2. Date of Service

Next, compare the dates shown on both documents.

Ask yourself:

Does the appointment date match?

Was I actually treated on this day?

Are multiple visits being combined?

If the dates don't line up, it doesn't automatically mean the bill is wrong, but it's worth asking for an explanation.

3. Provider Name

Make sure both documents refer to the same healthcare provider.

Remember that one hospital visit can generate bills from several different providers.

For example:

Hospital

Emergency physician

Radiologist

Laboratory

Anesthesiologist

Receiving multiple EOBs and multiple medical bills after one visit is often completely normal.

The important thing is making sure each bill matches the correct Explanation of Benefits.

4. Services Provided

Review the descriptions of the services on both documents.

Ask yourself:

Do these services generally match the care I received?

Is anything unfamiliar?

Are any services listed twice?

Don't worry if the wording isn't identical.

Insurance companies and providers sometimes describe the same service differently.

Instead, look for whether the overall care appears consistent.

5. Insurance Payment

One of the most important comparisons is the insurance payment.

Your provider should generally receive the same insurance payment shown on your Explanation of Benefits.

If your EOB says your insurance paid $1,250 but your provider's bill doesn't reflect that payment, contact the provider's billing office before paying.

Sometimes it's simply a timing issue.

Other times the provider may still be waiting for payment or may need to update your account.

6. Your Financial Responsibility

Now compare the amount your insurance company says you may owe with the balance shown on your medical bill.

Small differences can occur for legitimate reasons.

However, if there's a significant difference, don't assume either document is automatically correct.

Instead, ask your provider's billing office:

"Can you help me understand why my medical bill doesn't match my Explanation of Benefits?"

Often, the answer is straightforward.

Other times, it may uncover a billing issue that should be corrected.

7. Notes, Denials, and Adjustments

Finally, review any notes included on your Explanation of Benefits.

These often explain:

Why a claim was denied

Why additional documentation is needed

Why part of the bill wasn't covered

Why another insurance company should pay first

Whether your provider must adjust the bill

These comments may look technical, but they're often the key to understanding why your balance differs from what you expected.

What If Your Medical Bill Doesn't Match Your EOB?

Finding differences between your medical bill and your Explanation of Benefits doesn't automatically mean someone made a mistake.

There are several legitimate reasons why the amounts may differ.

For example:

Your provider corrected the claim after the original EOB was issued.

Your insurance company reprocessed the claim.

Multiple providers billed separately.

Additional services were submitted later.

A revised Explanation of Benefits is still being processed.

However, if you can't easily explain the difference, don't ignore it.

Contact your provider's billing office and ask for an explanation.

If necessary, contact your insurance company as well.

Most billing questions can be resolved with a simple conversation once everyone is looking at the same information.

A Quick Comparison Checklist

Before paying a medical bill, make sure you've compared:

✅ Patient name

✅ Date of service

✅ Provider name

✅ Services provided

✅ Insurance payment

✅ Patient responsibility

✅ Claim notes or denial explanations

Completing this review usually takes only a few minutes and can help you identify questions before sending a payment.

Key Takeaway

Your Explanation of Benefits and your medical bill are designed to work together.

Comparing both documents before paying gives you a better understanding of your healthcare costs and helps ensure the amount you're being asked to pay is consistent with how your insurance company processed the claim.

Common Explanation of Benefits (EOB) Mistakes and Red Flags

Most Explanation of Benefits statements are processed correctly.

However, healthcare billing is a complex process involving healthcare providers, insurance companies, billing systems, and coding specialists. With so many moving parts, mistakes can occasionally happen.

The good news is that your Explanation of Benefits gives you an opportunity to identify potential problems before paying a medical bill.

Here are some of the most common issues worth reviewing.

1. You Don't Recognize the Healthcare Provider

One of the first things to verify is the name of the healthcare provider that submitted the claim.

Sometimes you'll immediately recognize the provider.

Other times, the name may seem unfamiliar.

Before assuming something is wrong, remember that one medical visit can generate claims from multiple providers.

For example, a hospital stay might include separate claims from:

The hospital

The emergency physician

An anesthesiologist

A radiologist

A laboratory

A consulting specialist

If the provider name still doesn't make sense after considering your visit, contact your insurance company or the provider for clarification.

Red Flag

A provider you've never visited and can't reasonably connect to your medical care.

2. The Date of Service Is Incorrect

Compare the date shown on your Explanation of Benefits with your own records.

Ask yourself:

Was I actually seen on this date?

Does it match my appointment?

Was I hospitalized during this time?

A different date doesn't always indicate an error. Some services are billed on different dates than the actual office visit.

However, if the date seems completely unfamiliar, it's worth asking questions.

Red Flag

A date of service that doesn't correspond to any care you remember receiving.

3. The Services Don't Match Your Visit

Review the descriptions of the services that were billed.

They don't need to be identical to what you remember hearing in the doctor's office, but they should generally reflect the care you received.

For example, if you visited your doctor for a routine office appointment, seeing major surgical procedures listed would obviously deserve a closer look.

Red Flag

Services that seem unrelated to your visit or procedures you don't remember receiving.

4. Your Insurance Payment Doesn't Match Your Medical Bill

After your provider sends you a bill, compare it with your Explanation of Benefits.

If your EOB shows that your insurance company paid a certain amount, your provider's bill should generally reflect that payment.

Sometimes differences occur because:

The provider hasn't posted the insurance payment yet.

The claim was reprocessed.

Multiple claims are involved.

However, large unexplained differences deserve attention.

Red Flag

Your provider's bill appears to ignore or omit the insurance payment shown on your EOB.

5. The Claim Was Unexpectedly Denied

Seeing the word "Denied" on an Explanation of Benefits can be alarming.

Fortunately, a denial doesn't always mean you'll be responsible for the full amount.

Claims may be denied for reasons such as:

Missing information

Coding issues

Prior authorization requirements

Coordination of benefits questions

Administrative errors

Many denied claims are later corrected and successfully reprocessed.

Red Flag

A denial that isn't explained or doesn't seem consistent with your understanding of your insurance coverage.

6. The Provider Appears to Be Out of Network

Sometimes patients are surprised to discover that a claim was processed as out-of-network when they believed they were receiving in-network care.

There can be legitimate reasons for this.

For example:

A specialist practicing at an in-network hospital may not participate in your insurance network.

A laboratory may be out of network even if your physician is in network.

An ambulance provider may not participate with your insurance plan.

If this comes as a surprise, contact both your insurance company and the provider to better understand the situation.

Red Flag

You intentionally chose an in-network provider, but the claim appears to have been processed as out-of-network without a clear explanation.

7. Duplicate Claims

Occasionally, patients receive multiple Explanation of Benefits that appear very similar.

This doesn't necessarily mean you've been billed twice.

Sometimes:

A corrected claim replaces an earlier one.

Multiple providers billed separately.

The insurance company reprocessed the claim.

Before assuming duplicate billing, compare:

Claim numbers

Dates of service

Provider names

Services billed

Red Flag

The exact same provider, services, and dates appearing more than once without any explanation.

When Should You Ask Questions?

You don't need to investigate every small difference you notice.

However, it's usually worth contacting your provider or insurance company if:

You don't recognize the provider.

The dates don't make sense.

The services seem incorrect.

Your insurance payment doesn't match your bill.

Your claim was denied unexpectedly.

You can't understand why you're being asked to pay the amount listed.

Most billing questions have straightforward explanations, and asking early often makes resolving issues easier.

Remember: Not Every Difference Is a Mistake

One of the biggest misconceptions about medical billing is that every unexpected charge indicates an error.

That's simply not true.

Healthcare billing is complicated, and there are many legitimate reasons why an Explanation of Benefits and a medical bill may not look exactly the same.

The goal isn't to search for mistakes—it’s to understand your claim well enough to recognize when something deserves clarification.

Approaching the process with curiosity rather than suspicion will usually lead to more productive conversations with both your healthcare provider and your insurance company.

Key Takeaway

Most Explanation of Benefits statements are processed accurately, but reviewing yours carefully can help you identify situations that deserve a closer look.

If something doesn't seem right, don't ignore it—but don't assume it's an error, either. Ask questions, compare your documents, and seek clarification before making a payment if you're unsure.

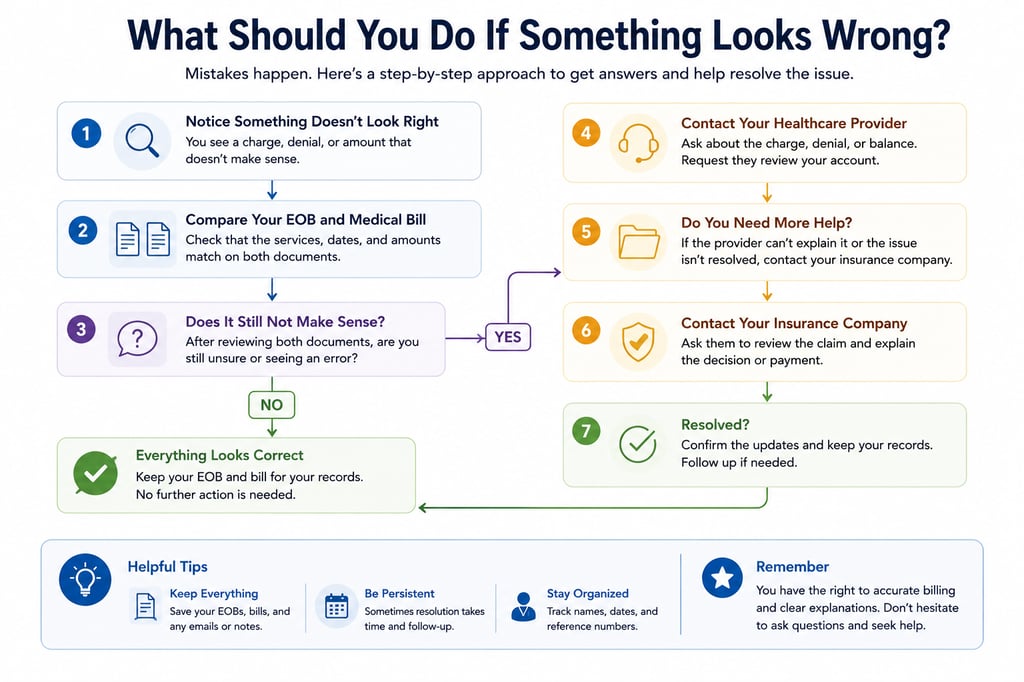

What Should You Do If Something Looks Wrong on Your Explanation of Benefits?

Discovering something unexpected on your Explanation of Benefits can be stressful. You may wonder whether you've been billed incorrectly, whether your insurance made a mistake, or whether you'll be responsible for paying more than you expected.

The good news is that many billing questions can be resolved with a simple phone call.

The key is to approach the situation methodically rather than assuming the worst.

If something on your Explanation of Benefits doesn't seem right, follow these steps.

Step 1: Compare Your EOB and Medical Bill

Before contacting anyone, place your Explanation of Benefits and your medical bill side by side.

Compare:

Patient name

Provider name

Date of service

Services performed

Insurance payment

Patient responsibility

Sometimes what initially looks like a mistake turns out to be a timing issue or a corrected claim.

Taking a few minutes to compare both documents can save you unnecessary phone calls.

Step 2: Gather Your Information

Before calling your insurance company or healthcare provider, have the following available:

Your Explanation of Benefits

Your medical bill

Your insurance ID card

Any previous correspondence related to the claim

A notebook or document to record the conversation

Being organized helps the conversation go more smoothly and makes it easier to reference details later if needed.

Step 3: Contact the Right Organization

One common mistake is calling the wrong office first.

Here's a simple rule:

Contact your healthcare provider if:

You have questions about the bill itself.

You don't recognize a charge.

Your bill doesn't reflect your insurance payment.

You need an itemized bill.

You want to discuss payment options or financial assistance.

Contact your insurance company if:

You don't understand your Explanation of Benefits.

You believe your claim was processed incorrectly.

Your claim was denied.

You have questions about your benefits or coverage.

You think the wrong deductible, copay, or coinsurance was applied.

If you're not sure who should answer your question, it's okay to start with either one. If necessary, they can usually point you in the right direction.

Step 4: Ask Specific Questions

Instead of saying:

"My bill is wrong."

Try asking specific questions such as:

"Can you help me understand this charge?"

"Can you explain why my Explanation of Benefits and medical bill are different?"

"Can you tell me why this claim was denied?"

"Can you explain how my patient responsibility was calculated?"

"Can you confirm that my insurance payment has been applied to my account?"

Specific questions are more likely to produce clear, helpful answers.

Step 5: Keep Records of Every Conversation

Whenever you speak with your insurance company or healthcare provider, keep a record of the conversation.

Write down:

Date and time

Name of the representative

Department

Phone number (if available)

Summary of what was discussed

Any next steps

Any confirmation or reference numbers

These notes can be incredibly helpful if you need to follow up later.

Step 6: Don't Ignore the Situation

Even if you believe a bill contains an error, avoid simply setting it aside and hoping it goes away.

Instead, contact the billing office and explain that you're reviewing the charges or waiting for your insurance company to resolve a claim issue.

Many healthcare providers are willing to note your account while an active billing question is being investigated.

Maintaining communication is often better than allowing the account to become overdue without explanation.

Step 7: Escalate When Necessary

If your initial phone call doesn't resolve the issue, don't be discouraged.

You may need to:

Ask for a supervisor.

Request a written explanation.

File an appeal with your insurance company if appropriate.

Ask your healthcare provider to review or correct the claim.

Request that the claim be resubmitted if additional information is needed.

Many billing issues are resolved only after additional review.

When Should You Consider Professional Help?

Sometimes the issue is straightforward and can be resolved with a single phone call.

Other situations are much more complicated.

For example:

Multiple providers submitted bills.

Your insurance denied a large claim.

You're receiving bills from collections.

You have several different medical bills to reconcile.

You're having difficulty understanding the documents you've received.

If you feel overwhelmed, don't hesitate to seek assistance.

Having someone help review your documents may provide clarity and help you better understand your options.

Key Takeaway

If something on your Explanation of Benefits doesn't look right, don't panic—and don't ignore it.

Compare your documents carefully, ask questions, keep records of your conversations, and work with your healthcare provider or insurance company to understand what's happening. Many issues can be resolved once everyone is reviewing the same information.

Frequently Asked Questions About Explanation of Benefits (EOBs)

1. What is an Explanation of Benefits (EOB)?

An Explanation of Benefits (EOB) is a document your health insurance company sends after processing a medical claim. It explains how the claim was handled, what your provider charged, what your insurance paid, and what portion of the costs you may be responsible for paying.

An EOB is not a bill. Instead, it's a summary of how your insurance benefits were applied.

2. Is an Explanation of Benefits the same as a medical bill?

No.

An Explanation of Benefits explains how your insurance company processed your claim.

A medical bill is a request for payment from your healthcare provider.

Although the two documents are related, they serve different purposes and should be reviewed together before you make a payment.

3. Why did I receive an EOB if I don't owe anything?

Even if your insurance covered the entire cost of your medical care, your insurance company may still send an Explanation of Benefits.

The purpose is to document how the claim was processed and show how your insurance benefits were applied.

Receiving an EOB doesn't necessarily mean you'll receive a bill.

4. Why did I receive an EOB but not a medical bill?

This is completely normal.

Many healthcare providers wait until your insurance finishes processing the claim before sending a bill.

In some cases, your insurance may have paid the entire balance, meaning you won't receive a bill at all.

5. Should I pay my medical bill before receiving my EOB?

If possible, it's generally a good idea to review your Explanation of Benefits before paying your medical bill.

Comparing the two documents helps confirm that your insurance processed the claim correctly and that the balance you're being asked to pay is consistent with your insurance company's records.

6. Why doesn't my medical bill match my Explanation of Benefits?

There are several possible reasons.

For example:

Your provider submitted a corrected claim.

Your insurance company reprocessed the claim.

Multiple providers billed separately.

The provider hasn't yet applied the insurance payment.

Additional services were billed later.

If the difference isn't clear, contact your provider's billing office and ask for an explanation before making a payment.

7. Can an Explanation of Benefits contain mistakes?

Yes.

Although most EOBs are processed correctly, errors can occur.

Examples include:

Incorrect patient information

Wrong dates of service

Claims processed under the wrong insurance plan

Unexpected claim denials

Duplicate claims

Incorrect provider information

Reviewing your EOB carefully can help you identify questions before paying a bill.

8. What should I do if I think my EOB is wrong?

Start by comparing your Explanation of Benefits with your medical bill.

If something still doesn't make sense, contact your healthcare provider or your insurance company and ask for clarification.

Many issues can be resolved once everyone reviews the same information.

9. What does "patient responsibility" mean?

Patient responsibility is the portion of the claim that your insurance company estimates you may owe.

It can include items such as deductibles, copays, coinsurance, or services that aren't covered by your health plan.

Remember that this amount is not a bill.

Your healthcare provider will determine the final balance you owe after insurance processing is complete.

10. Why does my EOB say my claim was denied?

A denied claim doesn't automatically mean you'll owe the full amount.

Claims can be denied for many reasons, including:

Missing information

Coding issues

Prior authorization requirements

Eligibility questions

Administrative errors

Some denied claims can be corrected and successfully reprocessed.

If your claim was denied, contact your insurance company to better understand the reason.

11. How long does it take to receive an Explanation of Benefits?

It varies.

Many insurance companies process routine claims within a few weeks, but the timeline depends on when your healthcare provider submits the claim and whether additional review is required.

If several weeks have passed and you haven't received an EOB, check your insurance company's online member portal or contact your insurer.

12. Can I receive multiple EOBs for the same medical visit?

Yes.

One medical visit may involve multiple healthcare providers.

For example, a hospital visit could generate separate claims from:

The hospital

An emergency physician

A radiologist

A laboratory

An anesthesiologist

Receiving multiple EOBs for the same date of service is often normal.

13. What is the difference between the Amount Billed and the Allowed Amount?

The Amount Billed is the amount your healthcare provider originally charged.

The Allowed Amount is the amount your insurance company recognizes under its agreement with the provider.

For in-network providers, the Allowed Amount is often significantly lower than the Amount Billed because insurance companies negotiate discounted rates.

14. What if I never receive an Explanation of Benefits?

If you expected an EOB but haven't received one:

Check your insurance company's online portal.

Verify that your provider submitted the claim.

Confirm your insurance information was correct.

Contact your insurance company for a status update.

Sometimes delays are simply administrative and can be resolved quickly.

15. What should I keep after my claim is processed?

It's a good idea to keep copies of:

Your Explanation of Benefits

Your medical bill

Any payment receipts

Letters from your insurance company

Notes from conversations with your provider or insurer

These records can be valuable if questions arise later.

Final Thoughts

Understanding your Explanation of Benefits may seem overwhelming at first, but once you know what you're looking for, it becomes one of the most valuable tools you have for understanding your healthcare costs.

Rather than viewing an EOB as just another piece of insurance paperwork, think of it as a roadmap. It shows how your health insurance company processed your claim, what your healthcare provider charged, what your insurance paid, and what portion of the costs you may be responsible for.

Before paying a medical bill, take a few minutes to compare it with your Explanation of Benefits. Confirm that the patient information, provider, dates of service, insurance payment, and estimated patient responsibility all make sense.

If something doesn't look right, don't ignore it—but don't assume the worst, either. Many billing questions have straightforward explanations, and asking questions early can often prevent larger problems later.

The more familiar you become with your Explanation of Benefits, the more confident you'll be when making decisions about your healthcare expenses.

Still Have Questions About Your Medical Bill?

Medical bills and insurance statements can be confusing, especially when the numbers don't seem to match or you're unsure what you're actually expected to pay.

If you're dealing with a confusing medical bill, have questions about your Explanation of Benefits, or simply want another set of eyes on your situation, Saventra is here to help.

Our free Medical Bill Assessment is designed to help you better understand your situation and determine whether we may be able to help.

During your free consultation, we'll:

Learn about your situation

Answer your questions

Explain whether we believe we can help

Walk you through the next steps if you decide to move forward

👉 Start Your Free Medical Bill Assessment

Related Guide

How to Read a Medical Bill: Everything You Need to Know

Learn how to read an itemized medical bill, understand common charges, and identify potential billing issues before you pay.

Last reviewed: July 2026

Disclaimer

This guide is provided for educational and informational purposes only and should not be considered legal, financial, insurance, tax, or medical advice. Every health insurance plan, medical bill, and healthcare situation is unique. If you have questions about your specific coverage, claim, or medical bill, contact your health insurance company, healthcare provider, or another qualified professional. Reading this guide does not create a client relationship with Saventra.